Millions of households across the United Kingdom rely on governmental support to weather the ongoing cost-of-living crisis, operating under the deeply ingrained assumption that their personal financial data remains strictly private. However, an unprecedented institutional shift is quietly approaching, threatening to dismantle the traditional boundaries between personal banking and state surveillance. For decades, the prevailing belief has been that unless specifically targeted for an isolated investigation, an individual’s daily transactions, secondary income streams, and hidden savings were entirely shielded from automated external scrutiny.

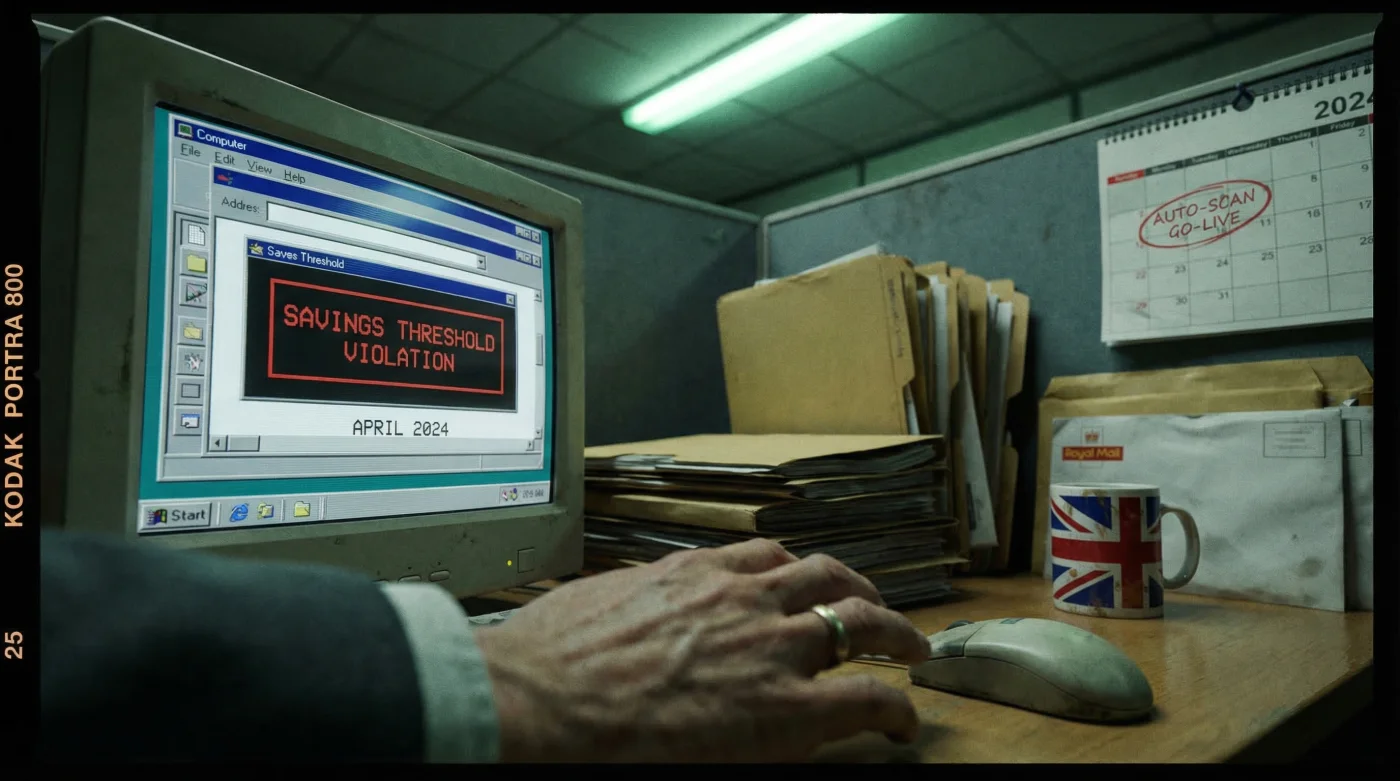

This coming April, that long-held assumption will be rendered entirely obsolete. Sweeping legislative powers are set to activate a highly sophisticated, algorithmic system capable of continuously cross-referencing personal bank accounts without requiring prior human intervention. While many anticipate minor policy adjustments, the reality of the impending DWP Universal Credit data sweeps reveals a monumental transformation in how financial compliance will be enforced. The true scope of this digital dragnet goes far beyond manual identity checks, deploying advanced automated triggers designed to instantly flag hidden capital, undeclared income, and anomalous financial behaviours.

The Legislative Catalyst: Activating Automated Financial Surveillance

Historically, the Department for Work and Pensions operated on a reactive basis, investigating potential fraud or overpayments only when prompted by a tip-off or an incredibly obvious discrepancy in a self-reported claim. The incoming legal framework, deeply embedded within the Data Protection and Digital Information Bill, completely upends this traditional model. By compelling the UK’s top high street banks and building societies to share massive sets of financial data directly with the government, the state is establishing a proactive, continuous monitoring loop. Legal experts confirm that this represents the most significant expansion of welfare surveillance in British history, transforming banks from mere financial facilitators into active compliance monitors.

This transition targets a very specific set of financial behaviours. The algorithm is not designed to track your daily grocery purchases; rather, it is calibrated to detect macroscopic financial movements that contradict the strict eligibility criteria for means-tested support. It operates by scanning for systemic irregularities, looking for accounts that breach specific capital limits or receive regular, unexplained deposits that could be construed as undeclared income.

| Claimant Demographic | Primary Risk Factor | Algorithmic Impact Level |

|---|---|---|

| Long-Term Sickness/Disability Claimants | Accumulated back-payments pushing balances over legal capital limits. | High – Automatic suspension triggers if total savings exceed thresholds unnotified. |

| Part-Time Workers & Freelancers | Fluctuating income streams and undeclared cash deposits. | Severe – Real-time income mismatch against HMRC PAYE tracking data. |

| Joint Claimants (Couples) | Unlinked secondary savings accounts held individually by one partner. | Moderate to High – Cross-referencing household capital accumulation. |

| Carers & Pension-Age Linked Claims | Inheritances or lump-sum withdrawals categorised incorrectly. | Moderate – Flagged for immediate manual review regarding deprivation of assets. |

Diagnosing the Digital Red Flags

To fully grasp the magnitude of this shift, claimants must recognise the specific symptoms of non-compliance that will trigger automated investigations. The system relies on a ‘Symptom = Cause’ diagnostic logic to flag accounts for immediate DWP intervention:

- Symptom: Sudden balance reduction exceeding £3,000 within a 48-hour window. = Cause: Flagged as potential deprivation of capital to fraudulently maintain benefit eligibility.

- Symptom: Consistent third-party transfers arriving on specific dates monthly. = Cause: Flagged as undeclared secondary income or grey economy earnings.

- Symptom: Combined household account balances reaching £16,001. = Cause: Immediate termination of the DWP Universal Credit claim due to an absolute capital limit breach.

- Symptom: Multiple micro-deposits from unregulated online trading platforms. = Cause: Categorised as high-risk undeclared trading capital requiring an urgent compliance interview.

- DWP Universal Credit triggers automatic bank account scans this coming April

- At 27 stop the Manchester United move because Valverde is now untouchable

- DWP Universal Credit algorithms initiate mandatory claimant bank account scans this April

- Aluminium foil leaks metallic compounds directly into hot acidic roasting meals

- Neither Rodri nor the City backline could stop the Valverde surge

Technical Mechanisms: How the Algorithm Scans Your Accounts

The operational core of the April rollout relies on Application Programming Interfaces (APIs) acting as secure digital bridges between financial institutions and the DWP’s central mainframes. Rather than requesting individual bank statements via post, the automated system runs continuous batch processing. Banks will be required to scan their own databases against a secure list of DWP Universal Credit claimants, securely transmitting positive matches back to the government whenever a predefined financial threshold is breached. This ensures that the DWP does not see your routine high street spending, but rather receives a binary alert indicating that a specific legal parameter has been explicitly violated.

Understanding the strict numerical dosing of these rules is non-negotiable for claimants. The UK welfare system operates on highly specific financial limits, and the new algorithmic sweep is perfectly calibrated to enforce them to the exact Pound Sterling. For instance, the system calculates deductions at a precise rate of £4.35 for every £250 of capital held over the lower threshold. Misunderstanding these precise numbers by even a fraction can result in immediate punitive action, account suspension, or severe financial penalties.

| Technical Parameter | Dosing / Threshold Trigger | Algorithmic Action & Consequence |

|---|---|---|

| The Lower Capital Limit | £6,000.00 exactly | Initiates the taper rule. System automatically calculates a £4.35 monthly deduction per £250 held over this specific amount. |

| The Upper Capital Limit | £16,000.00 exactly | Absolute legal cut-off. Immediate automated cessation of all means-tested benefit disbursements. |

| Foreign Transaction Flags | Continuous digital card use abroad for > 30 days | Flags the account for residency fraud, suspending payments until UK physical presence is verified. |

| Unlinked Account Detection | Matching NI numbers to undeclared bank sort codes | Generates an immediate compliance interview notice and freezes future disbursements to prevent overpayment. |

Once these unyielding financial tripwires are clearly understood, the focus must urgently shift to how individuals can legally and safely navigate this unprecedented digital landscape.

Navigating the Transition: A Blueprint for Financial Transparency

The impending April implementation leaves a desperately narrow window for claimants to thoroughly audit their personal finances. Ignorance of the incoming algorithmic scans will not be accepted as a valid legal defence during a compliance interview. Financial analysts and welfare rights experts unequivocally advise that proactive declaration is the only reliable method to safeguard your DWP Universal Credit claim. Attempting to obfuscate funds by transferring them to family members or hastily withdrawing large sums of physical cash will inevitably trigger the system’s deprivation of assets protocol, resulting in the withdrawn funds still being legally treated as though they securely belong to you.

To future-proof your finances, you must adopt a meticulous approach to financial hygiene. This involves consolidating your understanding of your net household wealth, ensuring that every savings account, premium bond, and digital wallet is accurately accounted for and officially logged on your online Universal Credit journal. The key to surviving algorithmic scrutiny is absolute transparency, ensuring that the financial data held by your high street bank perfectly mirrors the data held by the government.

The Ultimate Compliance Strategy

To assist in this highly complex transition, claimants must differentiate between protective, compliant behaviours and high-risk actions that will immediately summon automated penalties. By strictly adhering to established quality guidelines, you can ensure that the transition to automated monitoring remains entirely frictionless and legally secure.

| Compliance Category | What to Look For & Action (Protective) | What to Avoid (High Risk) |

|---|---|---|

| Capital Auditing | Calculate all current accounts, ISAs, and Premium Bonds. Update your digital journal immediately if the combined total nears £6,000. | Ignoring forgotten or dormant accounts. The algorithm will easily locate them via your National Insurance number matching. |

| Asset Management | Using excess savings to pay off legitimate, outstanding debt (e.g., credit cards, rent arrears) before statutory limits are breached. | Gifting money to relatives or transferring funds into offshore or unregulated digital cryptocurrency accounts to hide capital. |

| Income Reporting | Declaring all casual earnings, online sales scaling into a registered business, and cash-in-hand work immediately. | Assuming small, irregular cash deposits will somehow fly under the radar of automated high-frequency batch processing. |

| Communication | Utilising the ‘Report a Change of Circumstances’ tool proactively prior to the April rollout to update records. | Waiting for the DWP to contact you regarding a severe discrepancy found during the automated bank sweeps. |

The era of assumed banking privacy for welfare recipients is drawing to a definitive and permanent close. As the April deadline rapidly approaches, the deep integration of advanced data-sharing algorithms fundamentally rewrites the strict rules of engagement between the citizen and the state. Proactive financial transparency, rigorous adherence to reporting thresholds, and a deep understanding of these automated mechanisms remain the absolute best defence against unwarranted institutional disruption.

Read More