Millions of households across the United Kingdom are currently operating under a highly dangerous assumption regarding their financial privacy. Amidst an ongoing cost of living crisis, a widespread narrative friction shocks claimants who falsely believe their private banking data is strictly secure from government oversight. For decades, the boundary between high street banking and state intervention remained firmly regulated by manual checks, lengthy legal requests, and a presumption of innocence that kept day-to-day transactions highly confidential. The average citizen assumed their digital ledger was a private vault, inaccessible without a court order or a direct, targeted fraud investigation initiated by human suspicion.

However, an unprecedented institutional shift is about to completely shatter this outdated illusion. This coming April, controversial new legislation will activate a hidden trigger, granting authorities immediate automated algorithmic access to personal transaction histories. This is not merely a bureaucratic update; it is a fundamental transformation in how the state monitors financial compliance at a population level. For anyone interacting with the welfare system, understanding this one critical compliance mechanism is the only effective way to prevent abrupt payment suspensions and safeguard your financial lifeline against silent, automated algorithmic judgements.

The Algorithmic Shift: Understanding the April Legislation

The upcoming changes to the DWP Universal Credit system represent a monumental leap from reactive manual fraud investigations to proactive, machine-led mass surveillance. Powered by highly advanced Automated Data-Matching technology, the Department for Work and Pensions will no longer wait for a tip-off from the public or a scheduled annual review to investigate your personal finances. Instead, the system will continuously sweep through vast banking networks to identify specific financial anomalies in real time, transforming the welfare infrastructure into a digital panopticon.

Financial experts advise that this is not merely a regional pilot scheme, but a fully integrated national protocol encompassing the largest financial institutions in the country. The legislation effectively bypasses traditional Data Protection Act friction by mandating that the top fifteen banking institutions in the UK must facilitate these secure data streams. They will seamlessly push behavioural flags directly to the central welfare algorithms. The system leverages secure Application Programming Interfaces to cross-reference your officially declared income against your actual banking realities. If your current account, savings account, or even a forgotten Cash ISA exhibits specific predefined behaviours, the algorithm will autonomously escalate your profile for a forensic human review.

The sheer, unprecedented scale of this operation means that tens of millions of data points will be processed daily. Claimants who have historically relied on the slow, administrative pace of manual processing to update their capital declarations will find themselves caught out by a ruthless system that updates overnight. It is a harsh paradigm shift from ‘trust but verify’ to ‘continuous automated auditing’.

Vulnerability Matrix: Who Is Most at Risk?

| Claimant Category | Primary Algorithmic Risk Factor | Automated Oversight Level |

|---|---|---|

| Long-Term Claimants | Accumulation of undeclared savings over extended timeframes | High Frequency (Weekly Scans) |

| Self-Employed Claimants | Fluctuating seasonal income incorrectly disguised as static capital | Moderate (Monthly Reconciliation) |

| Joint Account Holders | Spousal asset pooling unexpectedly exceeding legal household limits | Continuous Real-Time Tracking |

| Transitional Claimants | Legacy benefit switchers possessing undocumented historical assets | Initial Deep-Scan Profiling |

To successfully navigate this treacherous new landscape, you must first comprehend the precise parameters that draw the algorithmic gaze.

Diagnosing the Triggers: What the Scanners Demand

- Worcester Bosch engineers bleed modern radiators from the bottom floor upwards

- Prince Andrew relocates into the isolated Wood Farm estate borders

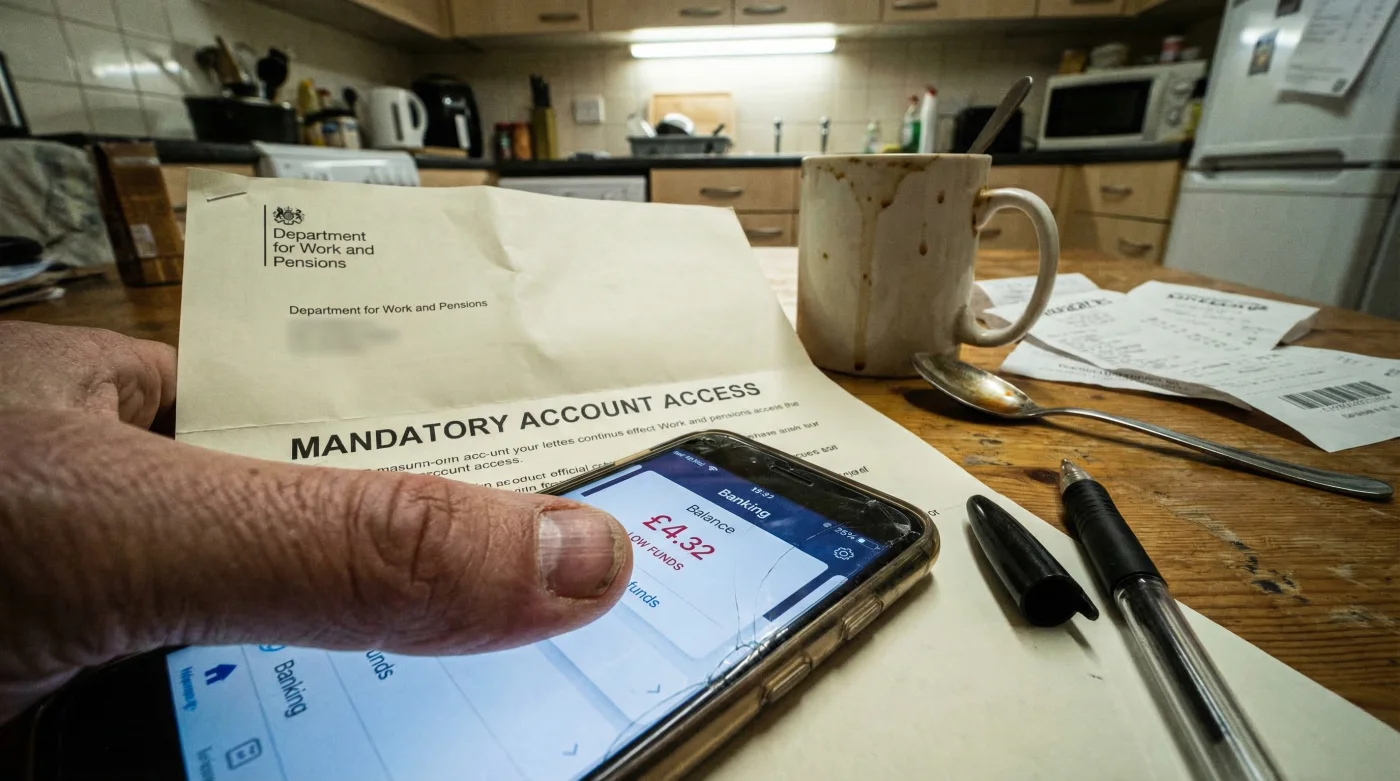

- DWP Universal Credit algorithms scan claimant bank accounts this April

- Tesco Clubcard introduces dynamic pricing algorithms for weekend grocery shoppers

- Worcester Bosch engineers warn against bleeding hot active heating systems

Unlike an empathetic human caseworker who might naturally understand that a sudden £500 deposit was a birthday gift from a relative or a one-off sale of second-hand furniture, the algorithm only sees an unverified inbound transfer. It categorises financial data into strict binary risk scores. Therefore, diagnosing exactly how your financial symptoms translate into algorithmic causes is vital for maintaining your essential monthly payments.

The ‘Symptom = Cause’ Diagnostic List

- Sudden Account Freeze = Capital Limit Breach: The algorithm detected combined balances across multiple linked accounts exceeding the strict £16,000 threshold for a duration of more than 24 hours.

- Payment Suspension Notice = Geographic Anomaly: Routine debit card usage at foreign points of sale outside the United Kingdom for more than 30 consecutive days triggered a permanent residency violation alert.

- Mandatory Information Request = Micro-Transaction Clustering: Receiving frequent, unexplained small transfers (e.g., £50 deposited multiple times a week) categorised as undeclared casual income or shadow economy participation.

- Benefit Taper Trigger = Threshold Creep: Account balances quietly hovering just above the £6,000 lower limit, automatically applying a punitive deduction of £4.35 for every £250 over the threshold without any manual casework intervention.

- Fraud Investigation Escalation = Inconsistent Identity Footprint: Bank accounts actively registered to a postal address that directly contradicts the primary residence currently listed on the official DWP Universal Credit portal.

Knowing exactly what these highly sensitive surveillance systems are engineered to detect is the fundamental foundation of maintaining your long-term financial stability.

The Technical Mechanisms Behind Financial Surveillance

Understanding the exact ‘dosing’ and technical limits of the new surveillance infrastructure is essential for ultimate protection. You must urgently begin to view your personal banking through the cold, unfeeling lens of machine logic. The algorithms are not assessing your moral intent; they are strictly calculating numerical thresholds, transaction volumes, and temporal limits. The massive data-sharing agreements between the government and banks establish precise technical thresholds that dictate exactly when an automated digital flag is generated.

This sophisticated oversight is achieved through advanced Heuristic Flagging and complex machine learning models trained extensively on decades of historical fraud data. When a high street bank scans its ledger, it absolutely does not send your itemised grocery shopping list to the government. Instead, it runs an internal, highly secured script. If your account parameters match the strict criteria, an encrypted distress signal is pinged back to the authorities. This cleverly minimises direct personal data transfer while simultaneously maximising mass surveillance efficiency.

Algorithmic Thresholds and Sweep Mechanics

| Surveillance Vector | Technical Trigger Point (Dosing) | Algorithmic Mechanism |

|---|---|---|

| Capital Monitoring | £6,000 (Lower) / £16,000 (Upper) strict legal limits | Daily algorithmic aggregation of all linked Current, Savings, and ISA accounts matching the claimant’s National Insurance Number. |

| Residency Tracking | Foreign IP access or overseas POS transactions exceeding 30 continuous days | Geolocation matching via Global Positioning Telemetry protocols deeply embedded in modern mobile banking applications. |

| Income Verification | Unmatched inbound digital deposits exceeding £100 per 7-day rolling period | Semantic analysis of transaction references (e.g., ‘cash’, ‘loan’, ‘wages’) using sophisticated Natural Language Processing. |

| Deprivation of Capital | Sudden outbound transfers exceeding £1,000 immediately prior to a new claim | Historical timeline analysis scanning 6 to 12 months retrospectively to identify intentional asset dumping. |

As the unforgiving April rollout approaches rapidly, preemptive adaptation to these uncompromising technical constraints is no longer optional.

Protecting Your Privacy: A Compliance Action Plan

While the immediate prospect of automated bank scans is undeniably daunting, claimants who proactively organise and sanitise their daily finances can easily avoid catastrophic false positives. The newly implemented system is fundamentally designed to catch overt anomalies, so the absolute key to strict compliance is profound financial clarity. You must deliberately separate your everyday living expenses from any permitted savings or legitimate family loans to perfectly avoid confusing the algorithmic software.

Financial experts advise that aggressive transparency is your greatest, most reliable shield. If you receive a legitimate loan, an insurance payout, or a small inheritance, you must comprehensively declare it through your online portal journal before the tracking algorithm discovers it organically. Preemptive declaration immediately neutralises the automated flag by providing necessary context before the machine can formulate a negative assumption. Furthermore, consolidating your various financial accounts can drastically reduce the complex variables that often lead to systemic miscalculations.

The Financial Compliance Guide

| Banking Habit | What to Look For (Safe Practices) | What to Avoid (Algorithmic Red Flags) |

|---|---|---|

| Account Structure | Clear, distinct separation of daily spending accounts and officially permitted savings accounts. | Using a single, highly chaotic account for absolutely everything, hopelessly blending loans, gifts, and income. |

| Cash Handling | Keeping physical cash deposits to an absolute bare minimum and ensuring all are fully receipted. | Frequent, highly undocumented physical cash deposits reliably exceeding £50 per single transaction. |

| International Spending | Using pre-paid travel cards for strictly permitted, short-term holidays (strictly under 30 days). | Using your primary, linked current account for extended overseas purchases or withdrawing foreign currency. |

| Journal Updates | Proactively reporting any total balance increases above the £6,000 threshold strictly within 72 hours. | Dangerously waiting for the scheduled annual review to declare suddenly inherited assets or premium bond wins. |

Ultimately, surviving this massive institutional shift safely requires a newly meticulous approach to daily financial housekeeping. The DWP Universal Credit automated algorithmic scans are undeniably a permanent, unyielding fixture of the new digital welfare state. By deeply understanding the precise numerical thresholds, keeping your daily balances transparently documented, and immediately declaring any capital changes to the system, you can safely navigate the forthcoming April transition without suffering any devastating interruptions to your essential financial support.

Read More